The opinions expressed in these forums do not represent those of C2, and any discussion of profit/loss

is not indicative of future performance or success.

There is a substantial risk of loss in trading. You should therefore carefully consider

whether such trading is suitable for you in light of your financial condition. You should read,

understand, and consider the Risk Disclosure Statement that is provided by your broker

before you consider trading. Most people who trade lose money.

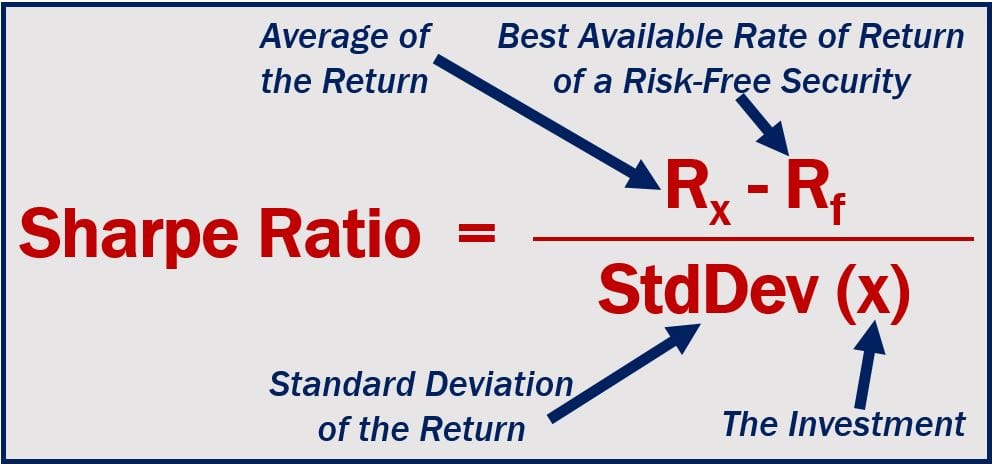

Also note that a standard deviation is just a number, for example here are 4 measurements :

15, 20, 25, 30

The standard deviation is simply 5.5901 (a number), regardless of what you are measuring.

And finally we can also express the monthly returns in percentage, it won’t matter, in both cases the sharpe ratio will be close to zero.

Most funds adopt CAR… Otherwise, which one are you using??? you just sum them up and divide them by 12 months??? Using CAR is the most appropriate way to calculate SR

It seems that there are many ways to calculate the sharpe ratio (SR) of a trading system.

How this SR is calculated on C2 is still unclear, as far as I can tell from these two Sharpe ratio topics :