Hey there, Collective2 Community!

Matthew gave me a unique opportunity to test the performance of smart portfolios on various ranking methods.

This thread will be dedicated to testing Smart Portfolios based on strategies from the C2Star Program.

If you haven’t heard about Smart Portfolios, check the link below:

https://collective2.com/smartportfolios

The main idea is that you choose the ranking method, set the conditions acceptable for your capital, rebalancing frequency, and then C2 automatically subscribes you to the Top N strategies every N days according to the selected rank method.

Of course, some natural questions arise:

- what are the risks?

- what are the returns?

- how long are portfolio drawdowns?

These questions I want to discuss in this thread.

Thread head is quite long, so I’ll start with what is inside:

- Portfolio backtest results based on the ranking of all C2Star Program strategies.

- Portfolio backtest results solely based on strategies that passed the C2Star Certification (Gold Star)

- Smart Portfolio generation on the Paper Account for real-time testing, and results update before each rebalance.

- Data collection methodology.

- Excel file with various portfolio sizes results (top 2, top 3, top 5, etc.) for individual reading.

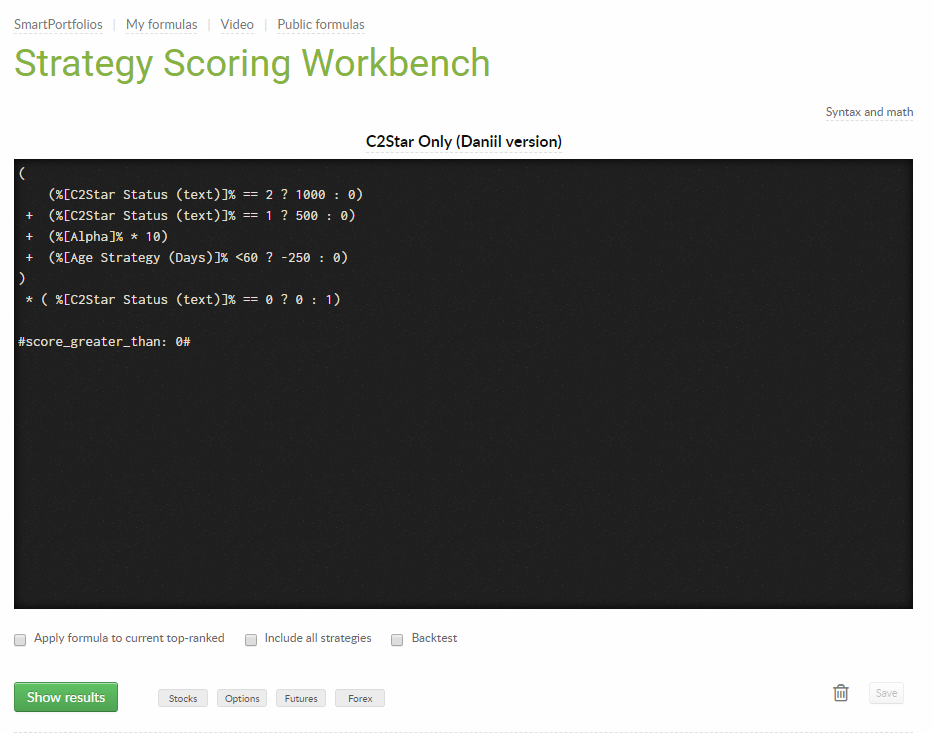

Smart portfolio based on the ranking of all strategies of C2Star Program.

I named this Rank method C2Star Only (Daniil version).

How the ranking works:

My formula is almost identical to the one written by Matthew, I just downgraded significance of the strategies with an age less than 60 days

This formula selects strategies in the C2Star certification program.

Sort order:

- first, full-certified (i.e. have met all criteria for sufficient time)

- second, in the program but have not yet achieved full certification with the age over 60 days

- third, new arrivals in the program (age less than 60 days)

Within these bands, strategies are ordered by Alpha (i.e. Alpha is the tie-breaker).

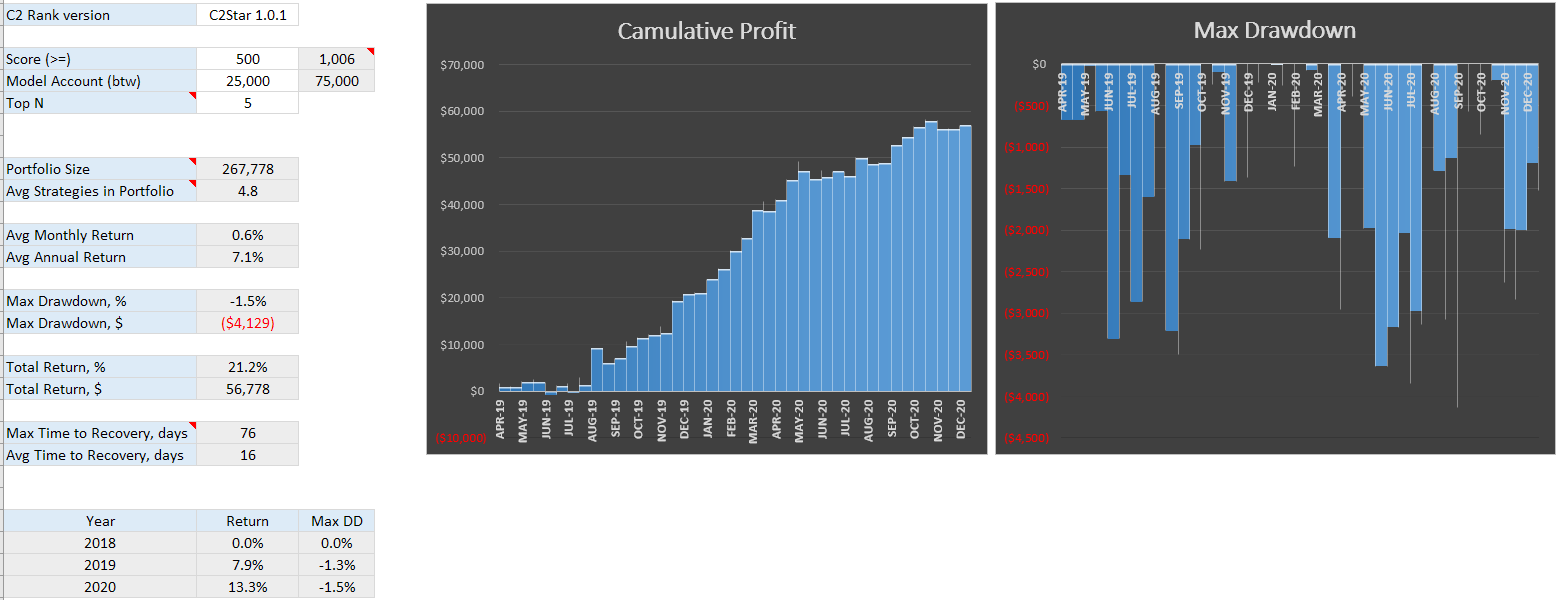

How the backtest works:

- Using the Scoring Workbench, I collect data of every 15 days and save it to a table. Data on the C2Star Program has been available since April 2019 (more in Data collection methodology section)

- I have made an Excel model to process this data, and it allows to:

- compose a portfolio of a different number of strategies

- set the model account size

- display performance results for a given portfolio

I believe that regardless of the backtests results, the optimal size of a smart portfolio is 3-5 strategies. This gives a good balance between risk diversification and capital in use.

Smart Portfolio backtest of 5 strategies by C2Star Only (Daniil version) Ranking Method.

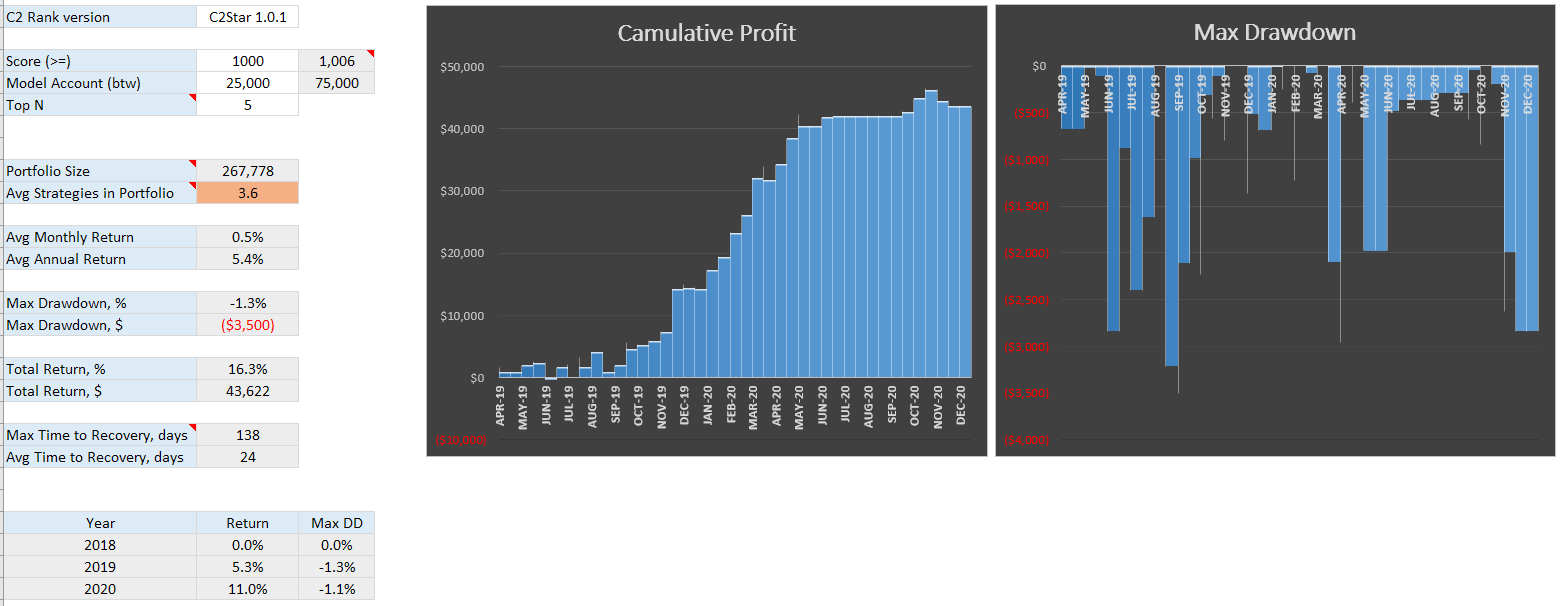

Smart Portfolio solely based on strategies that passed the C2Star certification conditions (Gold Star).

I named this Rank method C2Star Certificated Only by DaniilR.

How the ranking works:

- I take all strategies that have received Certified status in the C2Star Program.

- Sort by Alpha.

How the backtest works:

- Using the Scoring Workbench, I collect data of every 15 days and save it to a table. Data on the C2Star program has been available since April 2019.

- In Excel model, it is necessary to set the Score (>=) value of 1000. This will mean that only strategies that have received Certified status are considered in the portfolio generation.

Smart Portfolio backtest of 5 strategies by C2Star Certificated Only Ranking Method.

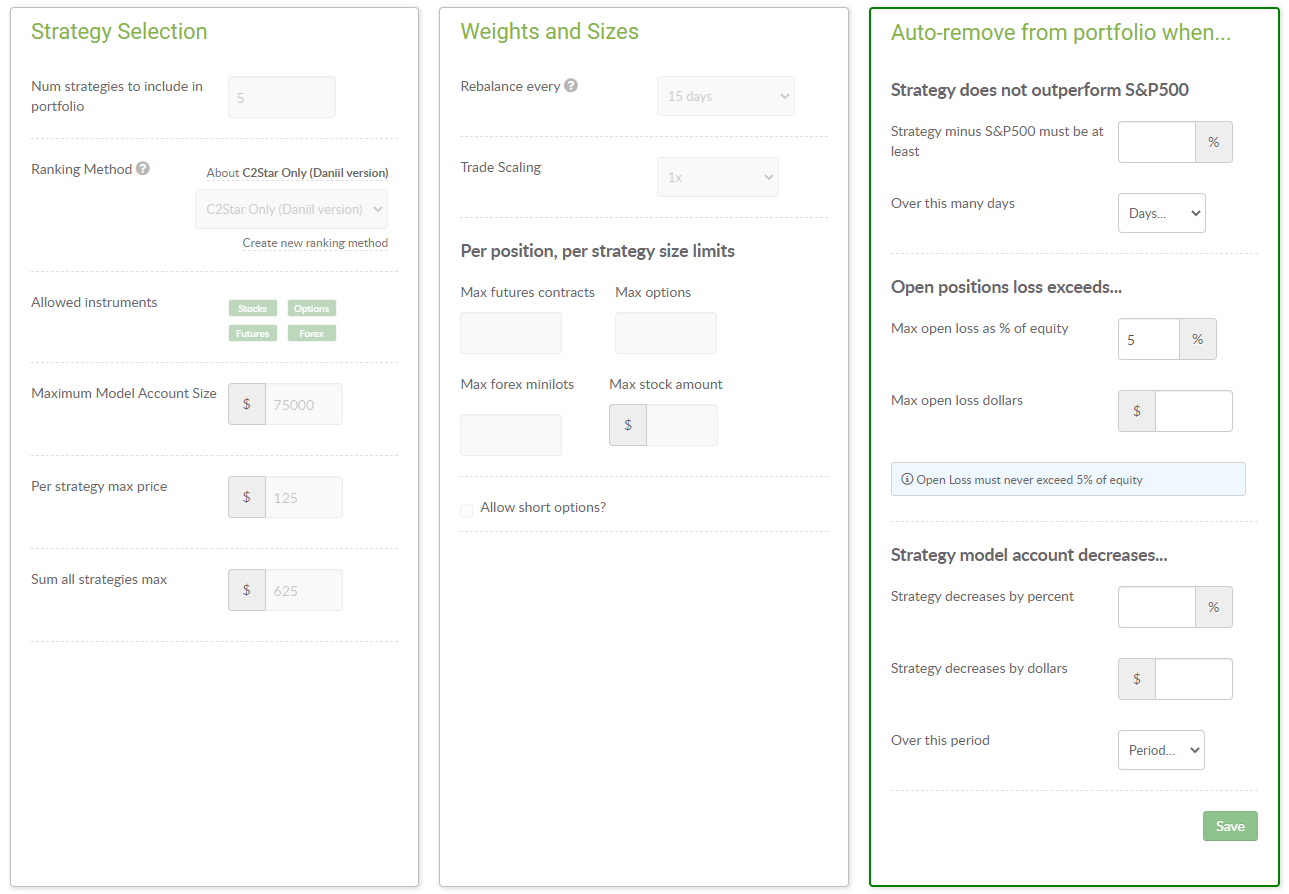

Smart Portfolio generation on the Paper Account for real-time testing.

C2Star Certification is dependent more on the behavior of SP500, when it falls, we have 10 gold star strategies, when it grows fast – none.

But being within the Certification Program imposes certain risk management rules on strategies, which affects their stability.

Judging by the backtests results, it makes no sense to limit the portfolio generation to strategies with a gold star, but to use all strategies in the Program.

As the result, on January 25, 2021 I created a Smart Portfolio on C2 Paper Account using the C2Star Only (Daniil version) Ranking Method.

Data collection methodology.

For those who want to do smart portfolios backtests themselves, I will demonstrate the easiest way to collect data that does not require any skills or special software.

All you need is access to the Scoring Workbench.

- Collect data

- Insert data to excel model

- Now you can start reading the results of various portfolios

Value Score (>=) is:

250 - the portfolio can be formed from all strategies of the program, including with an age of less than 60 days.

500 - the portfolio can be formed from all strategies in the program with an age of 60 days or more.

1000 - the portfolio is formed from full-certificated strategies (gold star) only.

Excel File with C2Star Smart Portfolio Backtest

It doesn’t work correctly in Google Sheets, use Excel.

Further in this thread, I will publish the result of this Smart Portfolio every 15 days. Let’s check it in real time.

I will be glad to get your feedback, do not hesitate to ask any questions.