Greetings, community!

Before I begin describing my research so far, let me first explain why I am working on this project. I am now part of C2’s still small (but hopefully growing) Quant Research Team. Matthew has asked me to analyze ways that investors can use C2’s data and tools to improve their investing using the C2 platform.

(While neither I nor C2 can guarantee that anything I write here will result in profitable trading, what follows is the result of some of my research so far.)

Ok, let’s start.

I often catch myself thinking “Just a little bit more improvements and ready to launch”. But then one week follows the other.

Enough of waiting! It’s time to launch and improve on the go.

I’d like to present you my ranking method: the idea, backtest method and launch of the SmartPortfolio simulation.

In this thread, I will publish the portfolio results after each rebalancing (every 15 days), and the backtest results of recent versions of the rank method.

Your comments and suggestions are appreciated, and the most interesting ones might be incorporated into the rank method development.

▌ Idea

I can’t provide the formula, as it will probably be used in future updates of C2Scoring, but I will try to convey its meaning.

I started with the idea that a trading strategy should be evaluated not by profitability metrics, but primarily by risk and behavior metrics. This will reveal antifragile strategies that are more stable. Therefore, this adds predictive value to the scoring.

In my work I use the powerful C2 Scoring Workbench tool.

There are various strategy stats available there, and developers constantly add new ones.

Based on these stats, I have created a set of my own metrics.

I have identified three groups of stats (I call them metrics): risk, behavior and profitability.

Each metric (stats group) can score a maximum of 33 points, which are evenly distributed among all the stats in the group.

Example

Risk metrics.

- Max Drawdown

- Max Open Loss for different periods of time

Behavior metrics.

- Strategy age

- Trades quantity

- Win month percentage

Profitability metrics.

- Alpha

- Sharpe Ratio

- Win month probability

▌ Backtest

Method

I used forward-backtesting at 15 days’ intervals (portfolio rebalancing every 15 days), resulting in 2 backtests per month, 24 per year.

Backrests’ period from Feb.2018 to Dec.2020.

In my Excel model, I considered the setting of stop loss by Max Drawdown and Max Open Loss.

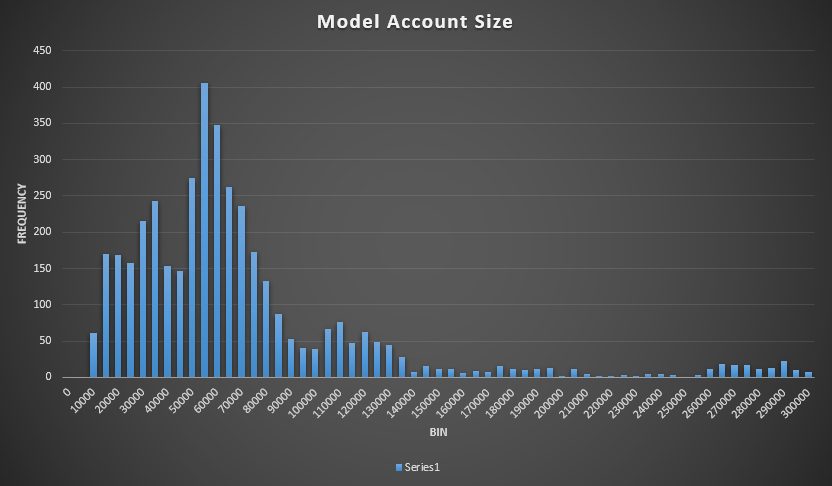

Strategy Model Account Size

The best Strategy Model Account Size in portfolio is between 40,000 and 70,000; I’ll explain it below.

I noticed that the best results come from portfolios where the Strategy Model Account Size (hereinafter SMAS) is between 25,000 and 75,000 and finally decided to find out why.

First, I plotted chart of the quantity of the strategy by SMAS

58.5% of strategies lie within the range from 25,000 to 75,000, which is not so much for the conclusion in favor of the quantity.

So, I plotted a chart of the quantity of the strategy that gained >= 90 scores (In my rank method maximum is 99) by SMAS.

82.5% of strategies lie within the range from 25,000 to 75,000.

76.2% within the range from 40,000 to 70,000.

This is already significant. I don’t know why this is, but it answers the question of why a portfolio in these ranges performs the best. It’s just that the best strategies are concentrated in this range.

Results

▌ SmartPortfolio launch

Based on the results of the backtest, I wanted to launch SmartPortfolio.

But since the minimum Strategy Model Account Size option has not yet implemented, the SmartPortfolio will be limited to only the maximum Strategy Model Account Size ($70,000).

For this scenario, the backtest looks like this

This variant is less balanced, since strategies with 20,000 and 70,000 can fall into the portfolio at the same time and their total contribution will differ. Nevertheless, it still looks like a working version. I’ll update it later when the Minimum Account Size option will be ready.

And so, from 03-May-2021 the Smart Portfolio is now up and running!

SmartPortfolio setup menu

↓

And Launched!

Here are the first five strategies selected by rank method DaniilR (v.2.3.5) for the next 15 days