Dear Matthew,

I’m posting this on behalf of a group of C2 Investors, who have collaborated online to help one another navigate the platform and find the best systems to follow. While complaints about the platform come up from time to time, I think we all can agree that Collective2 is second-to-none for finding, evaluating and trading others’ strategies across a broad spectrum of trading instruments.

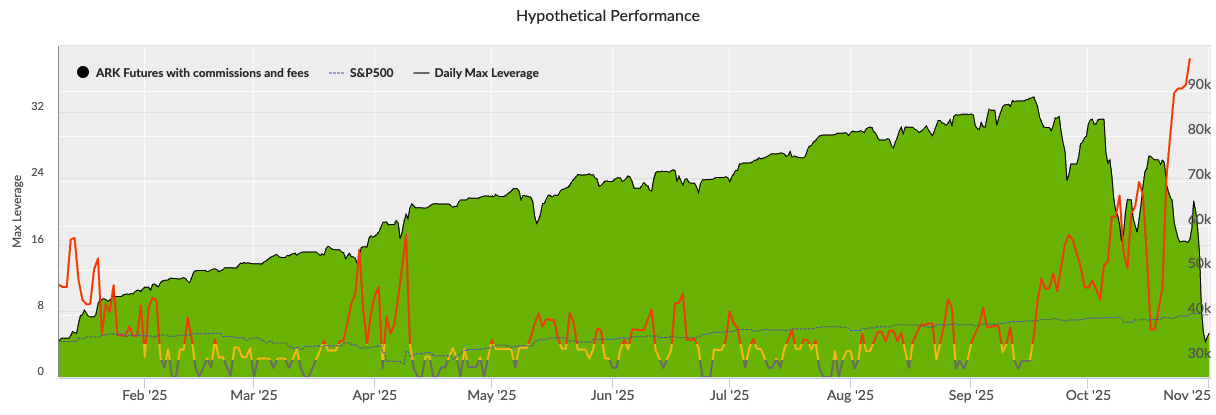

Many of us in the group feel that C2 could be doing more to protect subscribers, particularly newer ones, from high-risk strategies that are ticking time bombs. For experienced investors like us, we can look at the below chart and posted statistics to know that this ARK Futures system was a recipe for disaster:

Sure enough, it was:

This scenario has played out countless times over the years (several times from this particular manager), resulting in millions of dollars of subscriber losses. What’s the common thread? Martingale systems that use excessive leverage to recover from drawdowns until they hit a drawdown that they can’t recover from.

It is especially concerning when some Strategy Managers, such as ARK2, appear to be making a career by exploiting subscribers for several years (see forum posts from 2022 and 2024), rinsing-and-repeating new high-risk strategies one after another when they blow up.

What’s the solution? We came up with a couple of ideas:

-

Enforcing a leverage limit for non-TOS futures systems, such that trades that would result in surpassing the limit would be rejected. It is tricky, in that some legitimate systems trade with leverage as high as 20-to-1. Maybe the default limit could be 10-to-1 and managers could request a higher limit once they prove they need it.

-

Same idea as #1, but enforce the limit on the subscriber side. The default maximum leverage for autotrading a non-TOS futures system would be 10-to-1, which would ignore system trades that cause this limit to be breached. The user could choose to increase this limit (preferably with some sort of warning given when they do).

We understand that the risks taken are always the responsibility of the trader. However, we would like to see Collective2 take more explicit action to protect investors by making it more difficult for managers to blow their accounts by reckless trading and/or take advantage of subscribers through rinse-and-repeat risky strategies. We hope you will give these ideas some thought, and we would welcome hearing any other ideas that you or other readers of this forum might have to address this issue.

Thank you.

Collective2 Investors:

garylynn2

StuartS

BrianW_

Tweety

Adides

JITF

O_H

CraigW

Speculatius